Whew, what a quarter! As of our last full market commentary in January, the main stock market indexes were near record highs after more than a decade of gains. The conventional wisdom was that even though global manufacturing was in a recession, consumer spending in the U.S. would keep the economy afloat. Plus, the Federal Reserve would intervene, if necessary, to prevent any serious damage to financial markets. We were skeptical, as we often are. After asking whether market history still mattered, we concluded unequivocally that it did. Long periods of rising stock prices foster complacency, then overconfidence, then a vastly overpriced market, and finally a market bubble. Though it’s unpredictable what will eventually prick a bubble, bubbles invariably burst (popped by a global pandemic in this case). Accordingly, we continued to focus on capital preservation, both through asset allocation strategy and within stock market sectors.

How about that market!

Sure enough, the market peaked on February 19 and plunged 35% to March 23, perhaps the steepest drop on record. The bear market finally seems to have begun. As is normal after a sharp decline, there has been a sharp rebound (~25%) since then. The S&P 500 is now down only 19% from its February peak. Though each market cycle is distinct, we still expect the bear market to culminate in a decline of about 50% from the February peak (another 30% or so from here).

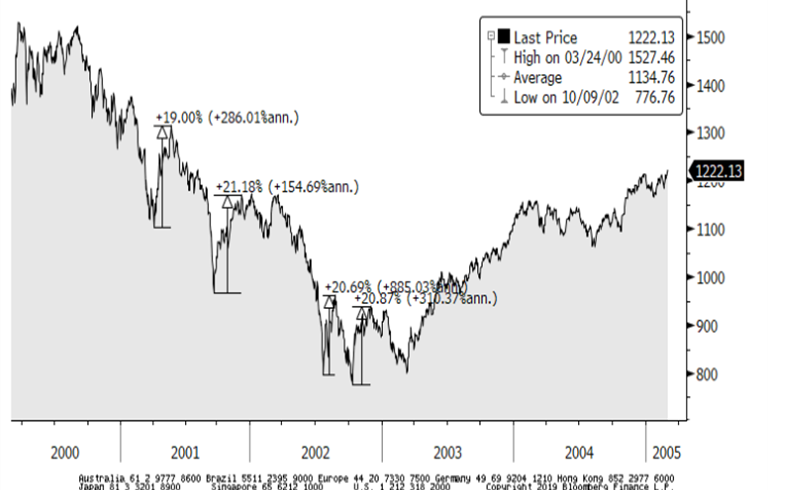

As Mark Twain supposedly said, “History doesn’t repeat itself, but it rhymes.” Major bear markets tend to fall between 45% and 55%. Within such a large decline, there are usually several substantial rebounds, despite economic and financial conditions that are obviously dire to most observers. Need to see it to believe it? Look at this chart to see that in the 2000-2002 bear market there were four strong market rebounds before we hit the real bottom.

We took advantage of the plunge in February and early March to scoop up some of our favorite stocks after declines of 30-50%. Now, with rebounds of 50-60% (and 150% in one case!), these stocks are much closer to our estimate of their fair value. That highlights the importance of being disciplined in setting buy points and sell points and not being swept up in the emotions of the moment.

When market sentiment is extreme, stock prices usually go the other way. We’ve seen it recently: Amid an extremely depressed investor mood, the announcement of record intervention by the Federal Reserve and signs of peaking Covid-19 cases sparked the biggest one-week gain in the S&P 500 since 1974. Investor sentiment rebounded along with stock prices and now is in neutral territory.

In our view, current stock prices now imply an overly rosy view of the potential for economic recovery during the second half of 2020. As more economic data emerges and as corporations begin to report the profound impact of the economic shutdown on their revenues and earnings, we think investors will be forced to reduce their expectations. That will likely lead to the next leg down in this bear market.

It’s the economy …

What about the prospects for economic recovery? As we’ve noted many times, the economy is a contrary indicator of future stock market returns, as strong economic conditions coincide with peak stock prices (and vice versa). It wasn’t long ago that unemployment was the lowest since 1968. How quickly things have changed. As one observer noted, “The global economy has essentially suffered a massive heart attack, we don’t know when it will recover, and the only thing we do know is that it will not be the same when it does.”

Many are hoping that the Federal Reserve will use monetary policy to help. After the 2008 financial crisis, not only did the Fed use its traditional tool of cutting short-term interest rates to stimulate borrowing, it intervened in markets to buy massive amounts of mortgage bonds, which injected money into financial markets and led to lower interest rates on home mortgages and other forms of debt. Unfortunately, the Fed didn’t return rates to their normal, higher levels after the economy recovered or sell off its bond holdings. In addition, given the Fed’s suppression of interest rates over the last decade, corporations have borrowed tremendous amounts of money (largely to repurchase their own stock in the stock market to boost share prices).

Now, with the economy the weakest since the Great Depression, the Fed’s short-term interest rate already is 0%, and it is printing a staggering amount of money to inject into the economy. Will this be effective? What unintended consequences might stem from this? In classical Keynesian economic theory, it is appropriate for governments to engage in deficit spending during economic recessions to stimulate demand. On the flip side, governments are supposed to build budget surpluses during strong economic conditions (the last surplus was under President Clinton in the late 1990s). Under Trump, the deficit was running at $1 trillion (almost 5% of GDP) before the economic collapse. The deficit might soar to 20% of GDP in the next two years. There must be a limit to this, but it’s global investors who will decide that.

Throughout world financial history, massive money printing has historically led to inflation—or hyperinflation in the case of Venezuela today and Germany in the 1920s. A new line of argument in the U.S., particularly among progressive economists, is that when a government borrows money in its own currency (as in the U.S.), it can always print more money to pay off its debts. So, major spending programs, such as Medicare for All, the Green New Deal, and cancelling student loan debt, could be paid for simply by printing more money. This is known as Modern Monetary Theory (MMT). Will this be effective or create massive inflation in the coming years? We will have more to say on this in an upcoming article.

Portfolio Management

In the meantime, after the sharp market rebound, we again are maintaining our strategic emphasis on capital preservation. This includes maximum cash levels, put options as a hedge (where clients see fit), and market sectors that are less volatile and which have relatively stable business prospects. Our favorites are communications services, consumer staples, health care, and real estate investment trusts (REITs). We expect continued extraordinary volatility in the market, both to the downside and to the upside (but with a strong bias to the downside). And as we said earlier, while we cannot predict the exact timing, we do expect one or more legs down in the market over the coming months. Put on your market seat belts, sit tight, and most importantly, stay well.